But, with new home sales in 2011 being 80 percent below the peak in 2005 (making the number of existing and new home sales the lowest in almost two decades), should bank marketers still invest in this target audience? Do consumers still spend at the same rate as in the past? Is this target audience even scaleable?

Interestingly, despite the ongoing reduction in home sales, the number of people moving has steadily increased since mid 2009, indicating that consumers in transition still represent both a risk and opportunity for marketers. In fact, the New Mover Report 2012 from Epsilon found that consumers continue to spend thousands of dollars in the months following a move, representing a valuable opportunity for those marketers who can identify and effectively communicate to new movers.

The study also found three major themes when they looked at consumer spending habits, brand affinity and channel preferences associated with a move from one location to another:

- Consumer brand loyalty is tested during a move, with new movers being twice as likely to change brands or service providers than non-movers.

- New movers have an interest in changing and/or upgrading services such as banking, credit cards and insurance after a move.

- Direct mail continues to be a highly valued channel for receiving information during a move, and is even highly valued by Gen Y consumers.

According to the U.S. Census Bureau, roughly 17% of Americans move each year, representing more than 53 million people. Those who move tend to be younger, with the distance of the move also being greater for younger demographic segments. The only exception being those households reaching retirement (around age 65) who also are more likely to move.

Research shows that while the economy is showing signs of slow and steady recovery, the volume of home sales continues to lag behind the highs achieved in the past. As a result, the ratio of renters on the move versus new homeowners continues to favor renters as it did in 2011. While this trend is not necessarily surprising given the scope of the housing market difficulties, marketers need to understand the difference between these two segments of movers as it relates to demographics, loyalty and purchasing behavior. The good news is that both new movers and home purchasers appear to be on the upswing.

The bad news is that as many as 33% of the people who move do not report their new address to the USPS (the central compiler of the National Change of Address (NCOA) file. As a result, targeting new movers (or even keeping a house file current) requires compiling multiple list sources including utility connections, phone changes, county records, etc.

Do Households on the Move Remain Brand Loyal?

Research shows that even when a household moves a short distance, marketers can't assume purchasing patterns will remain the same. According to the research done by Epsilon, brand loyalty is tested during a move, with the frequency of changing providers/brands being twice as likely for a new mover compared to a non-mover (some categories of services have a much higher propensity of change).

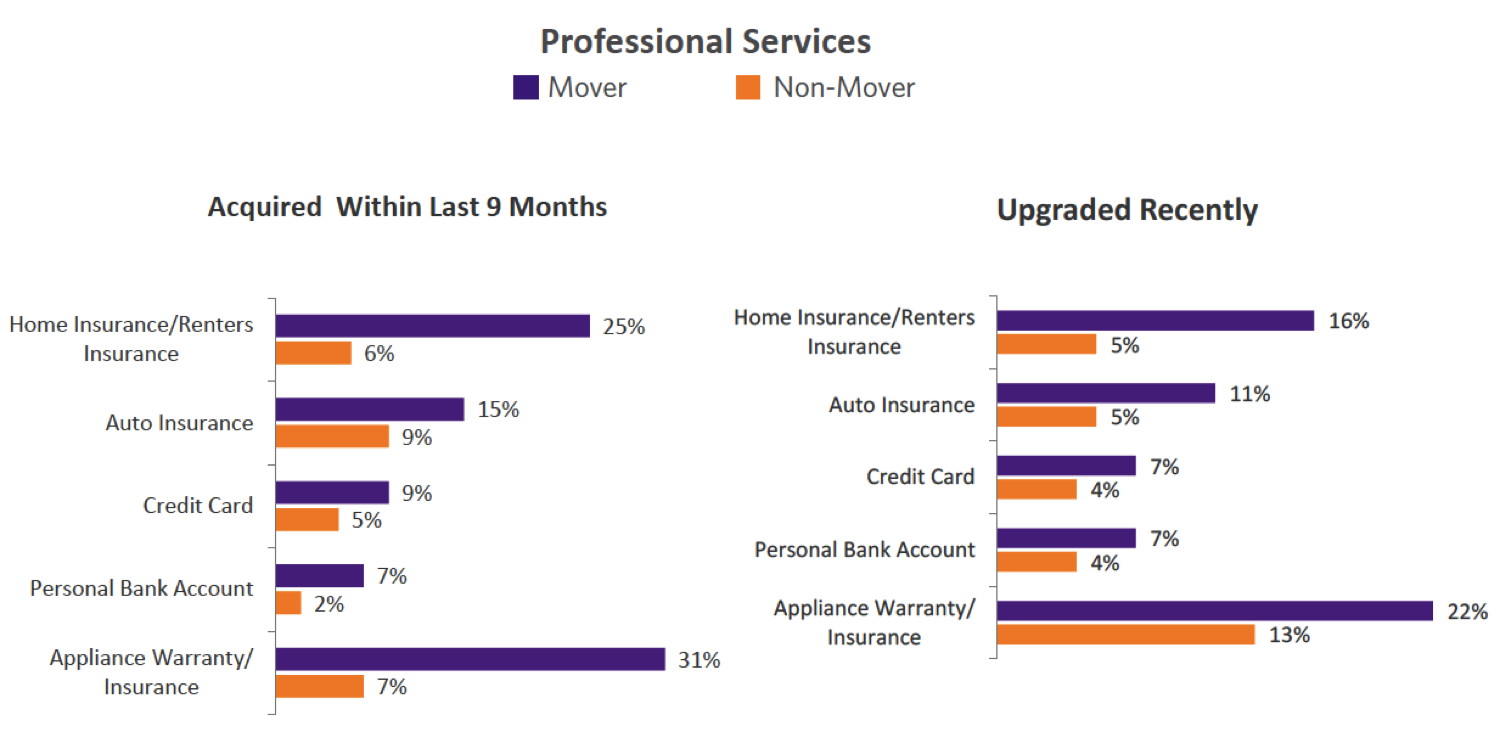

As shown below, some of the lowest levels of loyalty were in the category of professional services, where the difference in likelihood of changing brands between movers and non-movers were greatest for home insurance (3:1), auto insurance (2:1), credit cards (2:1), and banking accounts (3:1).

While a move, by itself, may not prompt a change in providers, it does appear to put loyalty to a specific brand or provider in play which indicates a defection risk for current customers and acquisition opportunity for prospects in a trade area.

When the research dug deeper into the reason for why movers changed brands, the overwhelming reason for change in the professional services category was the move itself (63%) compared to pricing (40%), service (19%) or any other feature/benefit offered.

Finally, beyond changing brands, new movers were also more likely to acquire or upgrade products and services in the professional services category. As was the case for the reason why movers switched brands, new movers indicated that the move itself as a major reason for acquiring or upgrading a professional service (59%), with pricing again being important but taking a back seat as a reason for upgrading (39%).

What Communication Channel(s) are Best?

As consumers use more and more channels to shop and buy services, it should be no surprise that a multichannel approach is recommended to connect with new movers related to retaining or acquiring households on the move. While there is very little disparity between the preferred channel of communication between movers and non-movers, word of mouth (referrals), email and direct mail are the channels most often mentioned as the way households want to learn about products and services.

It should be noted that recent research indicates the desire for direct mail being even more pronounced for the marketing of financial services as discussed in a number of previous blog posts including As Channel Proliferation Increases, Consumers Still Prefer and Trust Direct Mail for Financial Services Communication (December, 2011). This study also indicated a higher preference for direct mail among Gen Y consumers than for any other channel.

And while there is always a great deal of buzz among marketers around the use of social media, this channel is the least desired by both movers and non-movers. That said, social media should still be integrated as part of a marketing strategy since targeting new movers using social media will be much easier than with other channels such as mass media and email (due to list availability and accuracy).

Key Take-Aways for Marketers

As I mentioned in my previous post on the subject, Targeting New Movers for Enhanced Growth (February, 2010), the keys to reaching this transitional segment include:

- Be the first in the mailbox (or on the computer, phone or newspaper box) after a household moves to avoid clutter and benefit from early decisions

- Develop a system of immediate processing of prospects/customers to provide the foundation for being the first to reach the new mover in your category

- Measure the incremental impact of the program against your alternative acquisition/retention initiatives

The 2012 New Mover Report can be downloaded free of charge here.

Additional Insights:

U.S. Census Bureau Geographic Mobility/Migration Tables - December 2012

No comments:

Post a Comment