With continued rapid growth of both online and mobile banking, banks and credit unions need to come up with better ways of marketing through digital channels.

The technology is readily available, and best practices can be found at companies like Google, Amazon and others, but many banks are still at the infancy stage in terms of digital marketing capabilities.

To succeed in the future, financial institutions need to have a single view of the customer across channels, be equipped with advanced analytics for predicting behavior, be able to deliver offers to customers in real time and effectively integrate social media into the marketing mix.

A just released study by Efma and Wipro Technologies entitled, 'Global Retail Banking Digital Marketing Report', found that only a few banks are prepared for the digital marketing revolution, with the potential for improvement significant at most organizations. This first ever study also revealed that social media is not yet a part of mainstream marketing and is not a key customer interaction channel for most banks.

According to Rajan Kohli, vice president and head of banking and financial services at Wipro, "Digital technologies, social media and the explosion of data are redefining customer engagement models. The CMOs that we spoke with made it clear that the role of the CMO is changing as banks adapt to the development of new channels and capabilities."

For most banks surveyed, digital delivery channels were seen as complimentary to branches, being more important for processing transactions than for customer service and advice. With this transition across channels, it is believed interactions will be more frequent, insight collection will be more prolific and communication opportunities will be more direct.

As part of the Efma/Wipro study, a Digital Marketing Capability Index was created to benchmark capabilities vis-a-vis the best in class. Only 13 percent of banks surveyed demonstrated the highest level of maturity in digital marketing. The survey measured eight different capabilities including:

- Ability to get real time single customer view across channels

- Segmentation using customer lifetime value

- Ability to microsegment

- Availability of predictive analysis

- Real time, event driven marketing

- Personalization of offers on a 1:1 basis

- Implementation of test and learn approach

- Measurement of return on marketing investment (ROMI)

While banks in developed countries scored higher in most categories, key takeaways of the research illustrated the following potential for improvement:

- One of the weakest areas for banks is the ability to get a real time, single customer view of products held and transactions occurring across all channels.

- There was a surprising lack of test and learn processes and measurement of return on marketing investment in digital channels.

- While most banks are proficient at the use of advanced analytics (such as predictive analysis), most don't have the capability to integrate this insight in real time for marketing on a multichannel basis.

- While involvement in social media is standard practice at many banks, these channels are only used for outbound marketing and monitoring complaints. Using social media for transactions and digital interactions is lagging.

- Effectiveness of 'big data' projects (in the few places where implemented) has been modest, yet several of those surveyed believe big data will play a significant role in the future.

Interestingly, many smaller banks scored relatively well on digital marketing capabilities, possibly signaling an advantage of relatively new, non-legacy IT systems. The two direct only (online) banks in the survey both scored high in digital marketing capabilities.

Marketing Spend

The marketing mix at banks continues to change in response to the growth in digital channel usage. While the research indicated that traditional advertising comprises around 50% of a bank's marketing budget, this spend was less than 50% for banks in developed countries and as low as 20-25% of the budget at some of the more progressive banks surveyed.

When asked to project what the marketing mix will be in 5 years, traditional advertising and sponsorships continued to slide, with non-traditional (digital) and direct marketing increasing due to the potential for better targeting and measurement.

The Digital Marketing Capability Index

Using data collected from the survey, it was clear that big differences existed between the leaders and laggards in digital marketing. While significant work would be needed for many banks to reach 'best in class' status, the index provides a valuable index to measure opportunities for improvement.

Review of the actual study will provide additional insight into the measurement process and weightings, but a standard 'bell curve' was the 'digital maturity' output of measuring over 100 banks from 38 different counties from November 2012 and April 2013. Sixty-two percent of the responding banks were smaller banks, while 38% were medium/large institutions. Fifty-eight percent were from 'developing' countries with 42% being from higher income, developed countries.

Review of the actual study will provide additional insight into the measurement process and weightings, but a standard 'bell curve' was the 'digital maturity' output of measuring over 100 banks from 38 different counties from November 2012 and April 2013. Sixty-two percent of the responding banks were smaller banks, while 38% were medium/large institutions. Fifty-eight percent were from 'developing' countries with 42% being from higher income, developed countries.

As can be seen below, on average, banks feel most proficient at developing predictive analysis and segmentation. Deeper discussions with the banks in the study, however, indicated that very few banks are able to do analysis in real time or link the analysis back to individual customer offers on a channel level.

In addition, most banks fell short on the ability to leverage real-time, event driven marketing or 1:1 personalization which is becoming expected by customers in the digital age.

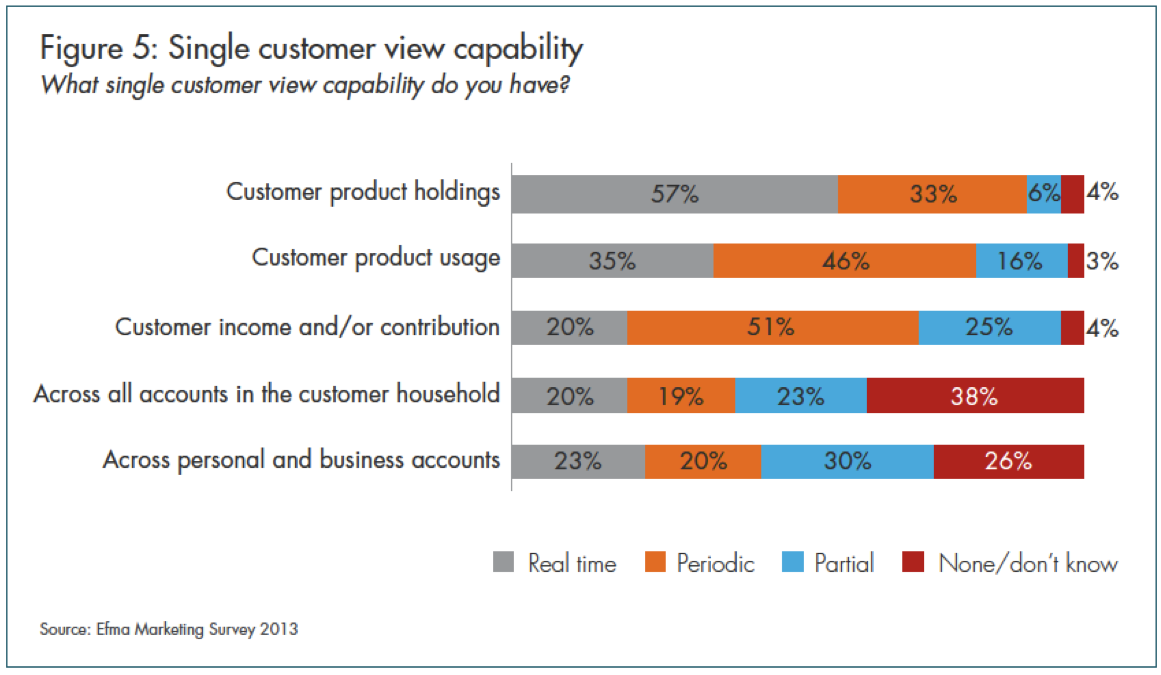

Real Time Single Customer View

Not surprisingly, most banks have a real time, or at the least a periodic, view of retail customer product holding, product use and transactions. What is less likely is for a bank to have a view of all accounts within a household or across business and personal accounts. All of these capabilities were projected to improve significantly over the next five years according to the study.

Segmentation

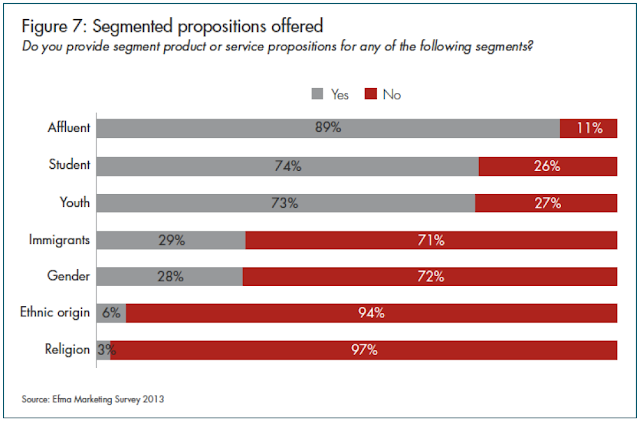

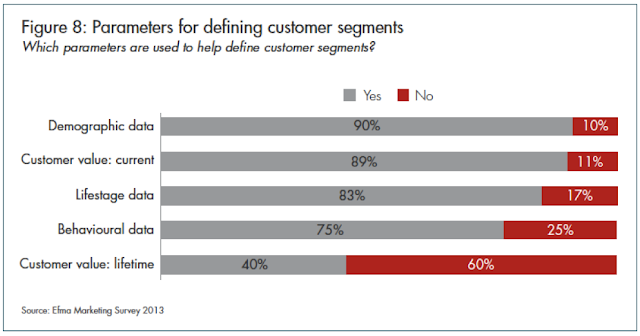

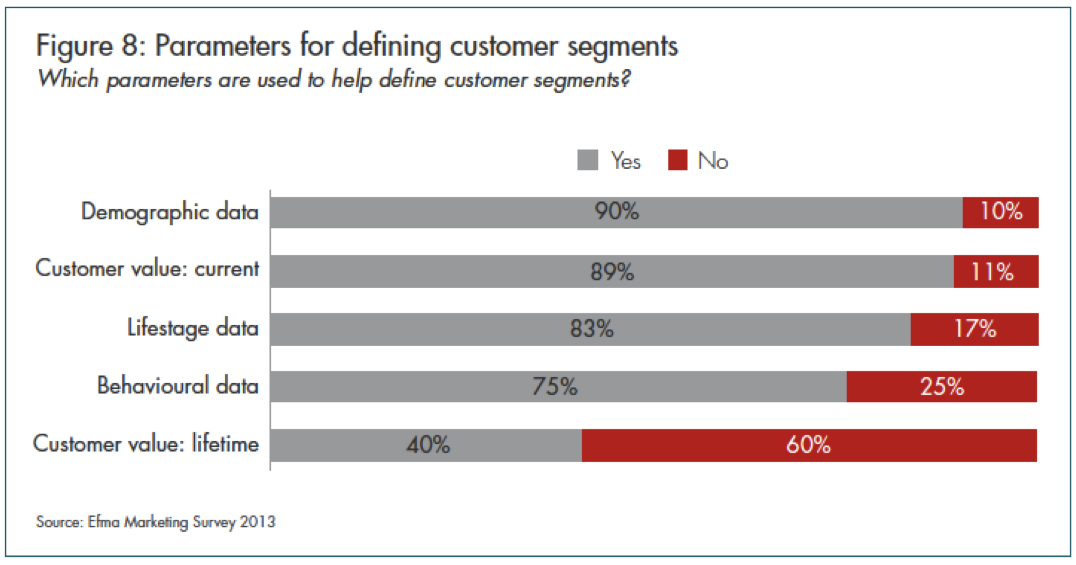

Segmentation for better targeting and customer experience is not new at banks or credit unions. In fact, 90% of the banks covered in the Efma/Wipro research are increasing their segmentation efforts to take into more detailed demographic categorization and even channel use. This is important since traditional demographic segmentation (age & income) has recently been found to have limited use. (see Bank Marketing Strategy coverage on the weakness of demographic segmentation here)

The missing element in many cases is lifetime value segmentation for use in dynamic, real-time marketing. In addition, online data such as web clicks and social media is still used rarely for segmentation purposes by banks while used extensively by other industries like retailing and travel.

Segmentation for better targeting and customer experience is not new at banks or credit unions. In fact, 90% of the banks covered in the Efma/Wipro research are increasing their segmentation efforts to take into more detailed demographic categorization and even channel use. This is important since traditional demographic segmentation (age & income) has recently been found to have limited use. (see Bank Marketing Strategy coverage on the weakness of demographic segmentation here)

The missing element in many cases is lifetime value segmentation for use in dynamic, real-time marketing. In addition, online data such as web clicks and social media is still used rarely for segmentation purposes by banks while used extensively by other industries like retailing and travel.

Business Intelligence

One of the more significant challenges for financial marketers today is the collection and analysis of unstructured data from within and outside the bank. As mentioned earlier, while predictive analysis was still found to be done in the majority of institutions, the use of this analysis to drive real-time decisioning was still rather rare. The same could be said for micro segmentation as shown below.

Real Time and 1:1 Personalization

The surprising lack of use of lifestage behavioral triggers and and 1:1 personalization of offers by financial institutions have both been covered recently by the Bank Marketing Strategy blog. The findings of the Efma and Wipro digital marketing capabilities study found the same deficit.

According to the study (and realizing that the numbers are marginally better in developing countries), only 36% of the banks can do any real time event marketing, and only 47% make 1:1 personalized offers.

Obviously, with more banking and credit union customers using online and mobile channels for the majority of their everyday banking, the inability to be agile with offers puts many banks at a disadvantage.

Test and Learn

The concept of 'test and learn' has been used in banking since the early 1980s, with large credit card companies being the earliest and most well known proponents of this strategy. More recently, other large banks, such as PNC, Chase, U.S Bank, Bank of America and others have integrated this technique as a standard operating procedure within their direct marketing and knowledge management teams.

Surprisingly, the global banking study found that 70% of banks reviewed use test and learn in less than 25% of their digital marketing campaigns, with only 10% of the banks using test and learn in more than 75% of their campaigns. Possibly more disturbing for seasoned financial direct marketing professionals would be the finding that while test and learn was used for individual programs, the findings were not retained and retested as part of an ongoing process.

Return on Marketing Investment

Despite the importance of measuring the results of marketing campaigns to justify future investment and determine which programs should be continued or curtailed, only 25% of the banks surveyed measured ROMI in more than 75% of their digital marketing campaigns. It was also found that the confidence in the measurements done was not high, potentially the result of different attribution strategies.

Interestingly, several of the banks surveyed also believed that almost all digital marketing campaigns were effective and that it was not necessary to measure the impact of any one campaign result. This is obviously a faulty assumption.

Social Media in Banking

It comes as no surprise to any financial marketer that the growth of social media has realized a parallel trend to digital marketing. Facebook, Twitter, YouTube, Pinterest, LinedIn and other popular social media sites have become the focus of discussion and debate within the financial industry as to the effective use and potential value of these channels. Adding to the confusion is the fact that most social media site users skew towards the younger demographic segments (that traditionally have a lower immediate value to banks and credit unions).

Because of this doubt, and despite a great deal of 'noise' that seems to point to the contrary, the spending on social media efforts by banks is still relatively small, with less than 500,000 Euros ($637K) being spent by 80% of the banks, with a very small number of banks spending over 1M Euros ($1.3M).

|

| 1M Euro = Approx. $1.3M |

Not surprisingly, Facebook continues to be the primary channel invested in by banks, followed by Twitter and YouTube. Interestingly, while user generated content was currently used least, this is an area of social media where more future investment seems to be heading.

Currently, social media is used more as a branding and broadcast communication tool and as a way to monitor customer comments and complaints. Despite some well documented successes in developing countries as well as in Australia and other countries overseas, most banks are not looking to social media as a transaction tool at this time. This may change as perceived security of these channels improves, but demand for integrated social banking does not appear to be strong in many countries.

Social Media 'Plateau' in Banking

Given the doubts surrounding the value of using social media extensively for bank marketing, the researchers involved in the Efma study believe the use of social media by banks has reached a 'plateau'. "While some banks are of course just catching up, the leading banks are still working out how to best use social channels in the future, conducting experiments, and looking for indicators from other industries," states Efma.

Other social media observations include:

- Social media is proving useful as a customer engagement tool.

- Most banks do not see social media as a strong ‘channel’ for product sales in the near future.

- Banks are considering using social media to ‘promote’ their services through advice and support, such as forums around house purchase

- Some banks are looking at how to make use social media for advocacy – using promoters to get positive messages out relating to new products or service

- Measurement of the effectiveness of spend on social media has been relatively basic, looking at high level metrics such as the number of “likes”on Facebook. (many banks are beginning to view these metrics as misleading)

- It is unlikely that most banks will try to offer transactional services through Facebook or Twitter in the near future, although some will make it possible to do small person-to-person payments to Facebook friends.

Note: A very detailed look at current social media initiatives globally is provided within the EFMA/Wipro research report available here.

Big Data in Banking

Despite a lot of noise and trade press that may give financial institutions the thought that they are 'falling behind' in the capture and use of 'big data' (no definition attempted here), the Efma/Wipro survey shows that only a few retail banks have begun to work on big data projects. Of those that have initiated big data projects, the effectiveness for increasing revenues or reducing costs is relatively modest so far.

In my travels across the country and in speaking to many marketers at some of the largest banks, it appears that most banks are using new technology to gather and analyze new 'small data' sources such as transactional data and money in / money out movements. While these would usually be considered 'structured' data uses, most banks want to maximize value of these data sources before tackling 'unstructured' data.

In other words, with digital marketing, social media marketing and big data, taking small steps may make sense before trying to 'boil an ocean'. The key is to not move too slowly . . . since the marketplace is moving at breakneck speed.

Additional Resources

'Global Retail Banking Digital Marketing Report' - Efma and Wipro (May 2013)

No comments:

Post a Comment