PAYMENTS STRATEGY

At a time when payment innovation seems like an everyday occurrence, it is exciting when new ideas come along that embrace both mobility and simplicity. In separate personal user tests, LoopPay allows me to make contactless payments at virtually every retail point-of-sale terminal while Square Cash enables me to collect money from friends with an email.

Here's why I no longer need a wallet filled with plastic.

When I initially covered these payments innovations in late 2013, both LoopPay and Square Cash drew my attention because of their unique strategies to impact the way people make payments. LoopPay promised to deliver a device that would 'trick' a traditional POS terminal into thinking a card was being used, making virtually every transaction contactless. Square Cash provided a secure method of making P2P payments via email. LoopPay's value proposition was to provide an easier and more secure way to pay merchants while Square Cash aimed to simplify P2P transactions.

Loop Wallet

Several weeks ago, I received my Loop Fob, the first in a series of Loop Wallet 'AppCessories' that would allow me to securely store and organize my payment, loyalty and gift cards in my iPhone while making contactless payments at more than 90% of today's terminals worldwide.

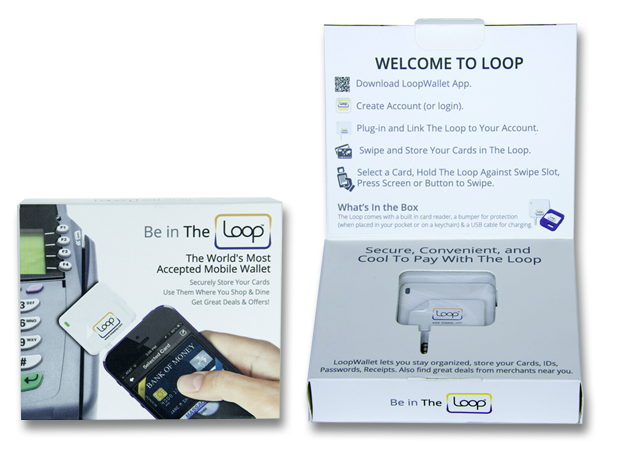

My first impression when I received my Loop Fob was that, while the packaging was very well done and provided a clear overview of what was needed to use the device, the device was larger than I anticipated. Once I began to use the device, however, I found the fob to be convenient while serving to whet my appetite for the soon to be released iPhone ChargeCase.

|

| The Loop Fob Wallet AppCessory Packaging |

Loop Wallet Set-Up

Once I downloaded the LoopWallet application from the iPhone store (Android version to be introduced shortly), I simply signed-up for the service and answered a series of security questions within the app. The securitization was complete after I entered an activation token that was sent to my connected email account.

Loading my cards was done using the card reading component of the fob while the fob was connected to my iPhone. A nice feature of the scanning process was the optional feature of adding a picture of my cards, the customer service phone numbers for for each card and an example of my signature. I could also add gift and loyalty cards as well as my drivers license to be part of my Loop Wallet.

The last step of the initialization process was to designate a default card that would be used when the fob is disconnected from my phone (the majority of my transactions have been with the fob disconnected). The default card can be changed at any time when the fob is connected to the phone. The tutorial below was a great way to understand the application process and usage of the Loop Fob.

Loop Wallet Application Introduction Tutorial

Loop Wallet Use

During several weeks of testing, I found the Loop Wallet to be better than expected. Except for gas station pumps and ATMs that are not currently supported by the app, I did not run into an instance that my Loop Fob didn't work. It was also nice that I could access all of my payment, loyalty and gift cards within the app as opposed to being limited to a specific number of cards (such as with the Coin mobile device).

That said, I did realize some of the challenges associated with any contactless payments process in the U.S., especially at sit down restaurants. In these locations, the card reading POS device is usually located either at a waitress station or in the kitchen. While I initially asked to walk back with the waiter, I quickly realized that doing quick training on the use of the fob was sufficient.

Overall, the best part of using the Loop Wallet was that virtually all POS terminals become contactless devices. So, while I am severely limited with the number of PayPass locations around my house, the number of traditional card readers (including PayPass locations) are virtually limitless.

The Future of Loop Wallet

According to Damien Balsan, EVP of LoopPay, the future of the Loop Wallet includes the introduction of an Android version of the LoopWallet application as well as the introduction of new payment devices including a phone case that will eliminate the need for the separate fob. Ultimately, LoopPay would like to partner with a financial institution, mobile carrier, etc. that would bring the benefits of the Loop Wallet within the phone itself.

When asked about the future of Loop Wallet in a world of NFC or EMV, Balsan said, "The industry is moving toward EMV, which will provide

substantial security for cards. It will take several years to build the necessary

infrastructure, however. Loop's secure technology can be implemented today. It is

security and mobile payments at zero cost to retailers."

Loop Wallet Security

A key feature of Loop's technology is that it adds substantial security to transactions. The security is based on tokenization, which makes part of the card data seemingly random and unusable to anyone else but the intended recipient. Stolen tokenized card data is useless for creating working counterfeit cards or transactions.

Called Partial Tokenization, it creates a new cryptographically generated token for each transaction. Since the key needed to create a valid token is not known, a counterfeiter is unable to create tokens for fraudulent cards or transactions. When loaded into the Loop Mobile Wallet, any existing magnetic stripe card can become enabled for secure tokenized transactions, provided the card issuer supports Partial Tokenization.

Because retailers do not need to upgrade their systems to support Loop, they can immediately benefit from its security features as can the consumer.

Square Cash

The second new payment application I tested was the new Square Cash request function. I have been an avid Square Cash user since it was introduced last year, paying family members, friends and service providers using email as opposed to writing checks. The immediacy and simplicity of this P2P solution is second to none, and each person who has received payment from me with this application has commented on how easy it is to use.

Building on the success of the initial Square Cash solution, Square recently expanded the capabilities of the application to include the capability to request funds in addition to sending cash. Similar to the process used to send money, I can now use an email to request funds from one or more people.

In my tests, I simply determined the amount of money I wanted to request from a friend, family member, etc. and used the app the same way I did when I sent money, except that I used the 'request' button (above). When I wanted to split a bill for a group gift, I entered the amount and multiple email addresses (the amounts need to be the same for a group email request).

Similar to a Square Cash payment, a Square Cash request sent an email to the designated people I wanted payment from and they made the payment using their debit card number. When they completed the payment, I was notified of the payment via email.

One great additional feature of the Square Cash request solution is a new page on the Square Cash website that tracked which of my friends or family had made a payment to me. This is great, especially for a person who already receives too many emails, making it difficult to remember who may be a deadbeat.

Beyond group gifts and meals, I can see this as a great application for those who regularly collect money for events, teams, etc. Square definitely makes the bookkeeping and anxiety of the collection process easier (reduced phone calls). The immediacy and ease of use makes this great for everyone.

Beyond group gifts and meals, I can see this as a great application for those who regularly collect money for events, teams, etc. Square definitely makes the bookkeeping and anxiety of the collection process easier (reduced phone calls). The immediacy and ease of use makes this great for everyone.

|

| Square Cash Request Status Page |

Dave Pogue from Yahoo discusses both the LoopPay device.

Additional Resources

Loop: The Future of Mobile Payments or a Temporary Fix? - Tech Crunch (Oct. 2013)

Square Cash Challenges Gmail With New Email Request Option - ZD Net (Feb 2014)

Square Turns On Money Request App - Mobile Payments Today (Feb 2014)

Square Cash Challenges Gmail With New Email Request Option - ZD Net (Feb 2014)

Square Turns On Money Request App - Mobile Payments Today (Feb 2014)

Mr. Balsan’s key statement is that Loop Wallet “is security and mobile payments at zero cost to retailers.” With the switch to EMV looming in the near future, at an estimated cost of $8 billion for replacing point-of-sale devices, credit and debit cards and upgrading ATM’s, the climate seems right for payments innovation. An example is PayPal’s Payment Code technology, which allows consumers to use QR codes or a one-time pin to make purchases using retailers’ existing infrastructure. The data breaches have created huge opportunity for creative start-ups like Loop to enter the payments market in a big way, and consumers are eagerly awaiting these innovations in payment security.

ReplyDelete