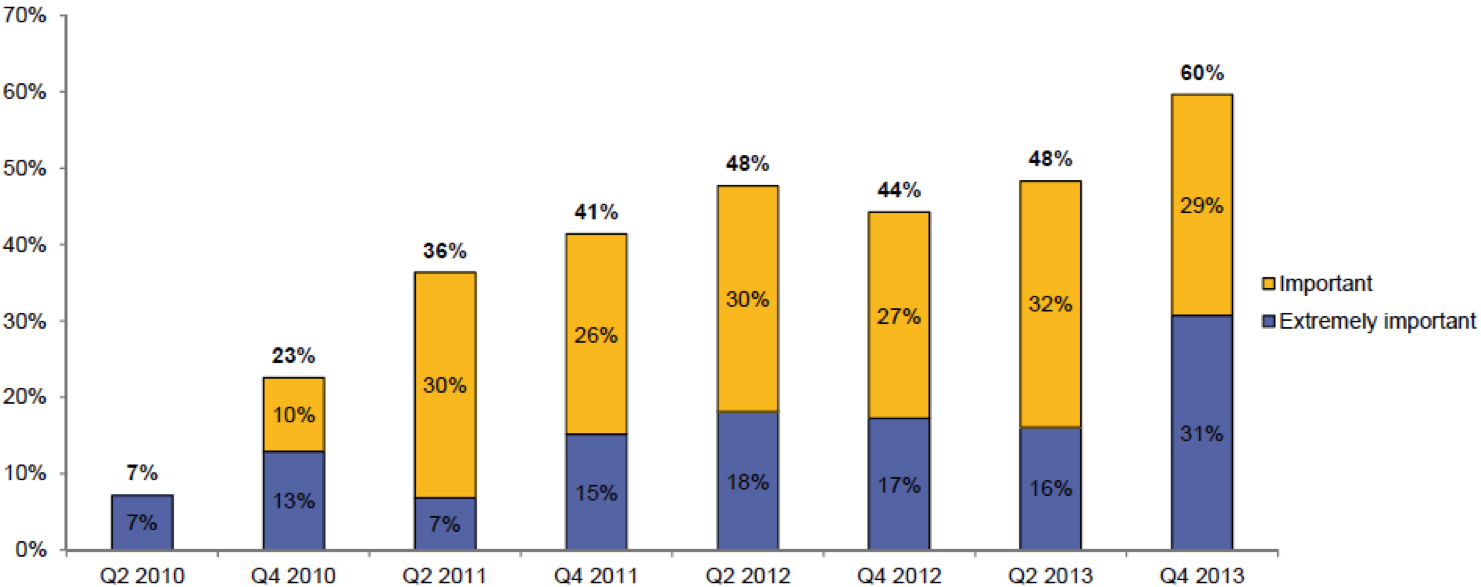

After a period of relative stability, the primary bank switching rate increased by more than 40 percent in late 2013, with 60 percent of smartphone/tablet users reporting mobile banking capabilities as being either "important" or "extremely important" in their decision to switch.

After a period of relative stability, the primary bank switching rate increased by more than 40 percent in late 2013, with 60 percent of smartphone/tablet users reporting mobile banking capabilities as being either "important" or "extremely important" in their decision to switch.

After relatively stable switching rates since the financial crisis, the number of consumers switching primary banks jumped from 7.1% in the first half of 2013 to 10% in the fourth quarter of 2013 according to the "Mobile Financial Services Tracking Study" from AlixPartners. This is the highest rate of switching since the end of 2008.

The highest incidence of primary bank switching was evident among millennials, where the annual switch rate approached 20 percent. The rate of switching quickly drops for older segments of the population, with baby boomers and seniors switching primary banks at low single figure annual rates.

|

| % Who Switch Primary Bank in Past Year Source: AlixPartners (March, 2014) |

|

| % Who Switched Primary Banks in Past Year by Age Source: AlixPartners (March, 2014) |

Among younger consumers, technology and innovation was of greatest importance, with the reasons for switching primary banks including:

- "My previous bank didn't offer the level of technology/innovation that I wanted"

- "My previous bank didn't offer the online services that I needed"

- "My previous bank didn't offer the mobile services that I needed"

For older consumers, the primary reasons for switching were because of a bad customer experience or because of a move, new job, etc.

Impact of Mobile Banking on Decision to Switch

Mobile banking is playing an increasingly important role in primary bank switching decisions, with 60 percent of smartphone and tablet users reporting that mobile banking capabilities are "important" or "extremely important" in the decision to switch. This compared to an already high 48 percent in a similar survey in the first half of 2013.

"The availability of mobile banking features plays an increasingly critical role in the consumer's decision to switch primary banks," according to Bob Hedges, managing director in AlixPartners' Financial Services Practice. "Consumers are demanding, expecting, and shopping for mobile capabilities. Banks who fail to innovate run the risk of losing customers and face real challenges in attracting new customers."

The importance of mobile banking capabilities in the decision to switch banks correlates with a strong growth in adoption of mobile services overall. According to the AlixPartners study, mobile banking is being used by 28 percent of U.S. banking consumers, up four percentage points from the survey in the first half of 2013, and up nine percentage points from the end of 2012.

As penetration of smartphones and tablet continue to rise and consumer adoption of mobile banking increases, the consumer's use of higher cost banking channels, such as traditional branches and live customer service call centers, appears to be declining. According to the study, mobile banking users reported visiting a bank branch 39 percent fewer times per month after adopting mobile banking services.

"The behavior and decision making of consumers who have adopted mobile is making the business case for mobile innovation and promotion by financial services institutions," added Hedges.

Digital Engagement Extends to Account Opening and Service Use

Consumer engagement with smartphones and other digital channels goes beyond the decision to switch primary banks. According to AlixPartners, 51 percent of younger switchers used online or telephone channels to open their new account in the second half of 2013, with only 35 percent using the branch for the entire account opening process (compared to 46 percent in the first half of 2013).

Further spotlighting the importance of digital innovation, mobile remote deposit capture (RDC) adoption is also growing steadily, with 22 percent of smartphone/tablet owners using the service compared to 18 percent in the first half of 2013. These users tend to be younger, wealthier and use more services at their primary bank than non-adopters.

"We will increasingly see banks developing and rolling out capabilities aimed at addressing specific consumer pain points and opportunities to add value. If mobile RDC is viewed as the current 'big attraction' in the ongoing wave of industry innovations on behalf of consumers, mobile photo bill pay could be the next big thing," says Epperson. "In the fourth quarter of 2013, 28 percent of consumers between the ages of 26 and 34 reported themselves to be likely to change banks to gain access to mobile photo bill pay," continued Epperson.

The Future of Digital Banking

All recent research studies point to a future of increasing mobile banking use and engagement. As sales of more technologically advanced mobile devices increase, consumers will become more comfortable with new applications that simplify daily life and provide tangible benefits.

In the future, consumers' mobile banking behavior and expectations will evolve rapidly. As a result, banks and credit unions will need to recognize the importance of rapid development and deployment cycles for mobile offerings in response to these expectations and understand that other industries, such as retail, may be setting the standard for new mobile offerings.

“As banks and other financial services providers explore new offerings that deliver value-added services to consumers, the growing importance of mobile capabilities in the lives of consumers should be viewed as both ‘table stakes’ and an opportunity for differentiation,” said Hedges. “Clearly, these devices’ extraordinary value to consumers has raised the bar on what consumers expect from their financial services providers and place greater importance on the role of mobile banking in bank selection. Those financial services providers that focus on mobile offerings as competitive differentiators will be winners in the future.”

The results of this survey are interesting. What interests me most is the sample AlixPartners used. Here is how they do it (from their website): The AlixPartners Mobile Financial Services Tracking Study is based on data collected in the fourth quarter of 2013, and is the latest edition in AlixPartners' semi-annual Franchise Health Survey, which has been conducted in the second and fourth quarters annually since 2008 and includes an online panel of nationally representative samples of U.S. consumers of at least 18 years of age.

ReplyDeleteWhat is clear to me is bank clients who like to respond to online survey's are at risk to switch banks due to mobile banking capabilities. What I would like to know more about is the behavior of the other group of bank clients and what it is that makes them switch.

More research is definitely needed to discover the root causes for bank switching today.

@dmgerbino

Great comments and clarification on the survey. While they definitely note that the switching numbers are for smartphone and tablet customers, they don't make a big deal that the comparison set is also 'online savvy' due to the surveying methods. As Ron Shevlin continues to emphasize, there is 'quantification' in every survey to some degree, but I am often frustrated by online surveys that leave less digital consumers out of the results.

ReplyDeleteAs with most surveys, we should probably look at comparison ratios as opposed to specific percentages and realize that the scalability of numbers may be smaller than we think. For instance, as opposed to the general population of smartphone/tablet owners (maybe 60%+ of the population), the survey is referencing those that also are online survey 'completers'. That said, the non-smartphone/tablet owners don't include those that don't own and are not comfortable with online surveys (more senior populations).

There will most likely be another research report that comes out next week that will refute some of these findings, but have another flaw in the survey methods.

Thanks David as always.