In an industry that is sometimes slow to innovate, Personal Financial Management (PFM) is one of the few banking applications where innovation has outpaced consumer demand. A 'hot' topic for over a decade, the ability to help consumers better manage their money through applied analytics, contextual design and visual tools has provided a battleground for financial institutions and direct-to-consumer applications.

With a quest to be at the center of account holder's lives, developers of PFM applications are moving from add-on applications to integrated solutions that can help define lifestyle segments. At the same time, the definition of PFM has evolved to include everything from basic visualizations to advanced engagement tools.

The question remains however . . . will these innovations capture the consumer's attention or simply be lipstick on the PFM pig?

In the newest in their PFM Insight Series entitled, Designing PFM Tools With The Customer in Mind, Mapa Research investigates the latest and most innovative PFM developments from around the world. Featuring in-depth quantitative and qualitative research from 60 banks, with examples from 23 banks and interviews from leading providers, the study hopes to provide guidance for banks and credit unions trying to decide if a business case for PFM can be made and if so, what should be the focus of development?

Building on the findings of the second edition report from Mapa Research entitled, Is PFM Still Worth Considering, the newest research found the following themes emerge:

- Customer centricity is as relevent as ever: A number of banks have integrated PFM within the overall digital experience, delivering added value through intuitive functionality.

- Leveraging new technology for cross-channel integration: While there are still only a few examples of exceptional integration across the online, tablet and mobile channels, more seamless tablet and mobile experiences are evident. Visuals have been improved, with more interactive tools including some available pre-login.

- Development and innovation must continue: For those banks and credit unions committed to PFM, more must be done to provide real time and even future views that help customers understand finances and improve their overall financial performance.

PFM offerings have expanded and have the potential to become increasingly important as a financial literacy tool, account aggregator, financial performance tool and in some cases, a non-interest income opportunity for banks and credit unions.

Acceptance of PFM

You'd think that with the rapid adoption of smartphone and tablet technology, people would quickly embrace digital money management. Especially given the fact that spending on the development of PFM tools is expected to double between 2010 and 2015, according to CEB research.

Nothing could be further from the truth according to recent research from Aite Group, Javelin Strategy and Research, Celent and Forrester. The challenge for banks and credit unions is that, in reality, most customers do not proactively monitor or manage their finances, and few look to their bank for support.

According to Ron Shevlin, senior analyst at Aite Group, "Almost half of Americans say they don't look to their primary financial institution for help managing their finances and therefore don't care if the FI offers tools to help them do so. In fact, 80 percent of households don't even do budgeting."

According to a September survey conducted by Aite Group, 58 percent of U.S. consumers have not used online PFM tools and don't plan to. Another 14 percent said they planned to do so, with 15 percent saying they use PFM tools exclusively at their bank or credit union site. The rest said they use a non-financial institution site or multiple sites. A Celent research report was even more dismal, with only 4 percent of online banking customers being active PFM users.

Interestingly, the percentage of users by age category in the Aite Group study skewed towards younger consumers, with 44 percent of PFM users coming from the Gen Y segment, 28 percent from Gen X, 16 percent being Baby Boomers and 15 percent being seniors. This may indicate the take-up of mobile tools is exceeding online PFM applications.

Nothing could be further from the truth according to recent research from Aite Group, Javelin Strategy and Research, Celent and Forrester. The challenge for banks and credit unions is that, in reality, most customers do not proactively monitor or manage their finances, and few look to their bank for support.

According to Ron Shevlin, senior analyst at Aite Group, "Almost half of Americans say they don't look to their primary financial institution for help managing their finances and therefore don't care if the FI offers tools to help them do so. In fact, 80 percent of households don't even do budgeting."

According to a September survey conducted by Aite Group, 58 percent of U.S. consumers have not used online PFM tools and don't plan to. Another 14 percent said they planned to do so, with 15 percent saying they use PFM tools exclusively at their bank or credit union site. The rest said they use a non-financial institution site or multiple sites. A Celent research report was even more dismal, with only 4 percent of online banking customers being active PFM users.

Interestingly, the percentage of users by age category in the Aite Group study skewed towards younger consumers, with 44 percent of PFM users coming from the Gen Y segment, 28 percent from Gen X, 16 percent being Baby Boomers and 15 percent being seniors. This may indicate the take-up of mobile tools is exceeding online PFM applications.

All of the recent studies point to the importance of integration of tools within current banking applications, ease of use, social media engagement, better mobile and tablet applications, and potentially rewards integration. If done well, PFM has been proven to be a gateway to deeper and more profitable relationships. The key, according to most studies, is to prove the value to the customer first and the value to the bank will follow.

"If you're looking to improve the relationship with the 80 percent (or more) of the households not fully engaged with PFM tools, you've got to rethink the definition of PFM and what's going to be offered," says Shevlin. As Shevlin wrote in a September 2012 Snarketing 2.0 blog post entitled, 'PFM is Dead, Long Live FPM', PFM should become FPM (Financial Performance Management), moving from 'oversight' (budgeting and expense) to 'insight' (how is money performing) and ultimately to 'foresight' (how can performance be improved).

Even then, a broad-based PFM (or FPM) may fall short according to JJ Hornblass, publisher of the Bank Innovation blog. "The problem is the lack of data, and the inability to tell a financial story beyond just one financial institution", says Hornblass. "PFM must tell the full data story. Until it does, only 27 percent of American consumers will find it "useful".

PFM Evolution

So, how are financial institutions and PFM vendors moving beyond the first generation of PFM offerings to be more valuable to the consumer and a better business case for the financial institution? How is PFM moving beyond 'slap on tools' to being integrated within products themselves? How is PFM being redefined to include benefits that the consumer will embrace?

According to the new findings from Mapa Research (executive summary of report available here), PFM offerings have become more diverse and that the redefinition (or breaking apart) of PFM components allows for a categorization of PFM functionality into three levels of progression as shown below:

- Basic Visualizations (Entice): Real-time feedback in relation to day-to-day finances including visualization of balances, transactions, etc.

- Analysis (Educate): How does customer spend/save relative to peers, categories, merchant, geolocation and holistic view of finances.

- Engagement Tools (Activate): Engaging tools to help customer improve financial situation through intelligent budgeting, goal development, forward-looking assessments.

With the progression above, the analysis of PFM functionality within this report illustrates a financial institution and vendor focus on improved simplicity, greater customer centricity and less 'friction' (seamless integration) between channels. In addition, greater attention to personalization and alert functionality was evident.

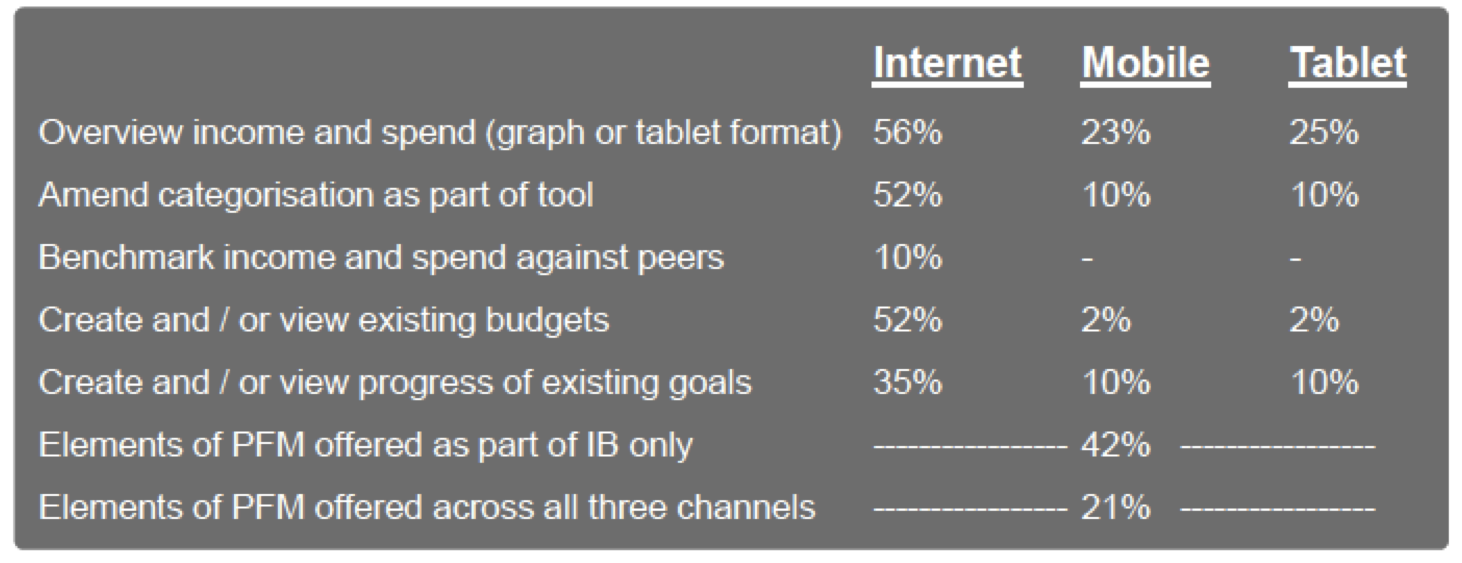

The current state-of-play was developed by reviewing 48 retail banks offering PFM tools across 10 countries. As can be seen, there continues to be opportunity to expand PFM capabilities across devices, with only 21 percent of banks surveyed offering PFM across all three channels.

|

| Source: Mapa Research (PFM Insight Series Edition #3; Designing PFM Tools With The Customer in Mind) |

Basic Visualizations

While basic visualizations are taking on many forms globally, there are some unique ways to illustrate basic balance and transaction insight, such as with BNP Paribas, where customers get an indication of their account status with weather visuals (sunny, cloudy or thunderstorm depending on account balance).

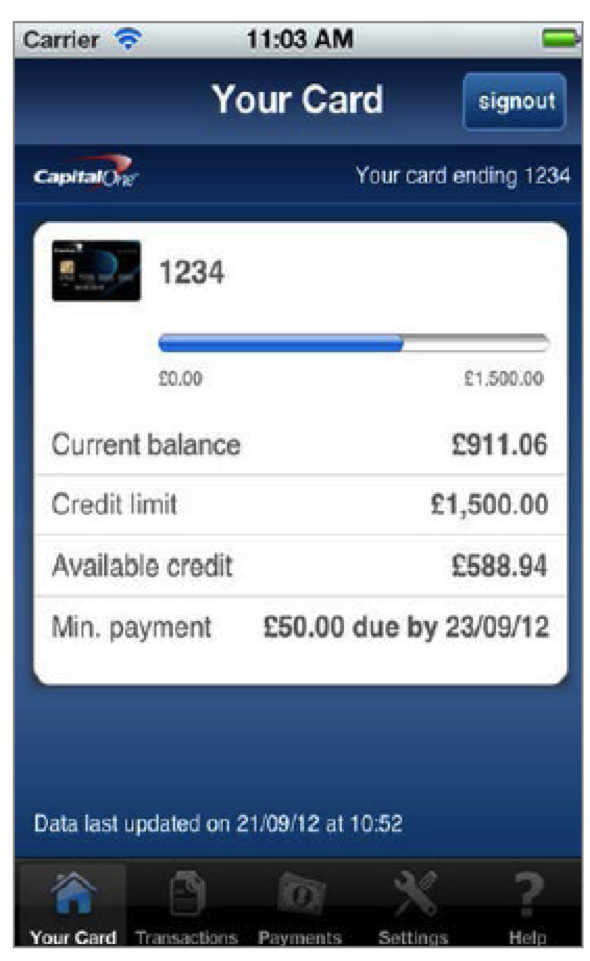

A number of banks, such as PNC, Capital One and Barclays Bank, use bar charts to indicate balances in different categories (spend, save, credit available, etc.) while some vendors, such as MoneyDesktop leverage bubbles to illustrate basic insights.

|

| Capital One (UK) |

Analysis

Similar to the analysis reports offered by investment firms for years, retail banking PFM analysis tools provide a rather extensive review of financial wellbeing using strong visuals and optional widgets for different types of information (inflows, outflows, goals, budgets, etc.). In most cases, the widget options are prominently displays so a customer can customize their financial analysis.

Because of the extensiveness of the information available for analysis, only a few institutions globally have a smartphone app for in-depth analysis. This insight usually is across the online and, on occasion, tablet platforms. Danske Bank was considered to be one of the best cross-platform applications for analysis, allowing customers to easily view money coming in or going out by category across all platforms.

Another example of an excellent analysis PFM application found by Mapa was at BNP Paribas, where great iPhone and iPad visuals are used to provide simple analysis capabilities that are easy to comprehend (even if you don't understand French).

|

| BNP Paribas (FR) |

Enabling customers to compare spend and allocation with peers is a way that could eventually improve a person's finances by seeing how they are doing compared with others like them. In Mapa research, examining 48 leading retail banks across 10 countries, four banks of the five banks globally (all Dutch) enable customers to compare spending with peers (and only within internet banking). OCBC (SG) is now providing this feature as an iPad application.

Take Action

The most frequently used technique for banks to encourage 'action' is by setting saving goals. It was found that not only was this functionality easy to set up and grasp by the customer, but it could be applied across all platforms relatively easily. In some cases, the sharing of savings goals could be done across social channels like Facebook, even enabling the customer to ask friends for contributions toward a goal.

In some cases, such as with Simple, a customer can divert funds from a goal to make the desired purchase, increasing the engagement and functionality of the 'goals' PFM tool.

One of the more unique capabilities within the 'action' category was ING's tool that allows customers to see how much could be saved over time by making small sacrifices. For instance, by using certain assumptions, a customer can see the impact of forgoing a cup of coffee, packing a lunch, walking to work, etc. With a simple click, the customer can redirect an amount they would have usually spent on an item to their savings account.

According to ING research, 52 percent of Canadians said that they could change their spending habits if they could visualize the impact of sacrificing non-essential purchases.

|

| ING 'Small Sacrifices' PFM Tool |

Dozens of illustrations from leading banks across the globe are available in the very extensive 56 page report on PFM developed by Mapa Research. The report includes commentary as well as vendor interviews around the future of PFM.

Increasing PFM Engagement

As mentioned, getting customers to use the new tools that have been developed and are continuing to be innovated remains a challenge. Each of the PFM vendors interviewed for the Mapa report (Yodlee, Figlo, Meniga, Strands Finance) and subsequent to the publishing of this report (MoneyDesktop and Geezeo) emphasized their commitment to greater enrollment and engagement (beyond trying to get banks and credit unions to offer PFM services).

Innovative approaches used to improve use and engagement of PFM tools by Mapa Research included:

- Seamless integration within regular banking services: Optional PFM add-ons will not be embraced by a populace that doesn't like budgeting. Instead, functionality should be part of the digital experience.

- Intuitive and pleasing visuals: To appeal to a broad customer base, the PFM tools should be easy to understand and highly visual.

- Segmentation of base: Instead of a one-size-fits-all approach, PFM features should be aligned with different segments of the customer base (mass, affluent, Gen X, Gen Y, investors, etc.)

- Make it social: Allow users to engage with others through social platforms. It was found that this was effective when building and sticking to goals even though the integration of social channels and banking is by no means commonplace in the U.S.

- Provide encouragement: People respond to ongoing encouragement and instant feedback. Moven is a great example of a bank that provides this form of engagement.

- Leverage Big Data: As mentioned by JJ Hornblass as well as reports from Cap Gemini and others, data must be leveraged more effectively to combine overall financial relationships, better understand customer needs and build engagement.

|

| Moven Immediate Feedback to Generate Engagement and Encouragement |

PFM Vendor Perspectives

To better understand recent and future developments in the PFM category, Mapa Research interviewed four PFM vendors in the development of the report (Figlo, Meniga, Strands Finance and Yodlee). In addition, I supplemented these interviews by allowing two additional vendors (Geezeo and MoneyDesktop) to provide insights to the same questions advanced by Mapa Research. A full copy of the questions and responses from Mapa are available in the appendix of the report.

Recent Developments

All six vendors questioned indicated a very similar emphasis around where current efforts are focused. The key areas of development included:

- Tighter integration of PFM functionality within current banking functions

- Focus on mobile and tablet platforms

- Better use of data for budgets

- More financial analysis and forecasting

- Ability for improved aggregation and categorization

- Better goal and advice functionality (including buy/no buy decisioning tools)

- Increased segmentation and customization (including small business)

- Better marketing capabilities within offering

- Alert functionality

Common Objection From Banks Around Implementing PFM

The PFM vendors were asked what banks view as the primary stumbling block to the implementation of a PFM solution.

- Lack of internal resources to implement and deliver a PFM solution

- Lack of proven demand, ROI and business case support

- Internal development of primary PFM functionality

- Internal data issues (inability to consolidate customer information)

How Can Customer Adoption Rates Be Improved

Each vendor in the survey as well as the two additional vendors I interviewed agreed with many of the ways that can improve customer adoption and engagement.

- Improved training of the front line

- Proactive marketing of the service through direct and digital channels

- Online videos illustrating benefits and use

- Simplify and improve UX/UI all components of PFM for the customer

- Move beyond online platform to mobile and tablet

- Target potential user groups

Evolution of PFM Over Next 12 Months

The vendors were asked how PFM will evolve and how consumers will/or won't embrace PFM in the future.

- Better cross-channel integration

- Better data integration

- Better insight and analytics moving towards 'tool of empowerment'

- Continuous enhancement of user experience (simplicity)

- Segment-based PFM (small business, wealth management)

- Potential as fee-based service

Lipstick on the PFM Pig or a Brand New Pig?

After years of simply trying to take an overarching money management concept and add more and more functionality (PFM lipstick), it appears that the PFM marketplace is beginning to take specific components of personal financial management apart and integrate the tools within the banking services. In other words, instead of focusing on putting PFM on steroids, banks, credit unions and vendors are finding ways to bring the benefits of money management within the platforms and accounts in a more simplified manner.

More importantly, PFM is becoming part of what banking is in real time. And instead of being only a rearview mirror view of finances, tomorrow's PFM will look ahead with advice as to how to prepare for the future and provide 'foresight' for a stronger financial well being.

It appears that the biggest change around the definition of PFM is that bigger may not be better after all. Instead, the original concept of PFM is being broken down into easier to swallow pieces of insight that are more desired and more valuable to the consumer and the bank.

Maybe we have moved from putting lipstick on the PFM pig to serving delicious pieces of PFM bacon, sausage, pork chops, etc. The question may now become . . . will the consumer pay for these new treats?

Additional Insight

PFM Insight Series Edition #3; Designing PFM Tools With The Customer in Mind - Mapa Research (August 2013)

PFM Insight Series Edition #2: Is PFM Still Worth Considering - Mapa Research (June 2012)

PFM Insight Series Edition #2: Is PFM Still Worth Considering - Mapa Research (June 2012)

Strategies for PFM Success - Aite Group (Sept. 2012)

PFM is Dead, Long Live FPM - Snarketing 2.0 (September 2012)

PFM is Dead, Long Live FPM - Snarketing 2.0 (September 2012)

Personal Financial Management (PFM) 4.0 - Online Banking Report (June 2012)

Personal Financial Management 2011 - Javelin Strategy and Research (December 2011)

Personal Financial Management: Five Things FIs Need to Do in 2011 - Yodlee & Javelin Strategy and Research (January 2011)

The paradigm shift we are starting to see is the shift in development from 'bolt on' apps to integrated tools that are part of the products being developed. Moven, Simple, GoBank and many banks overseas have realized that the masses don't want an accounting software application app in addition to their checking account.

ReplyDeleteThey want a checking account (or credit card) that tells them their current (and future) financial scenario when they do a transaction . . . in real time. The problem is that as an industry, we continue to view PFM as charts, graphs and analysis instead of realizing that being able to tell me that I have spent more in a category than I have historically or that I shouldn't make a major purchase because my normal inflows and outflows won't support it is what the New PFM is all about.

Not only do the vendors need to put on a new set of PFM glasses, the bankers do also so that we don't continually view PFM as Mint, Quicken, etc. Instead of the 'next big thing', PFM in the future will be the real time integration of smaller PFM elements that we see every day. This simplified mobile-first, with online as the back-up deeper dive for those interested.